Thinking of investing in healthcare REIT in this current Covid-19 environment? Over the past few months, the global economy has been adversely impacted by the Covid-19 pandemic. Almost every sector is affected including the REIT sector. We have seen many businesses shutting down and some taking drastic measure to help weather the economic storm.

Though that is the case, a number of sector continues to thrive during this economic condition. One of the recent ones is the glove manufacturing sector. The question is, how does healthcare REIT hold on amidst this pandemic?

In this post today, we will be looking at Parkway Life REIT, the largest healthcare REIT in Singapore. We will look at its historical performance over the past few years as well as their performance in the first half of 2020 amidst the pandemic.

Historical Performance

To help gauge the performance of Parkway Life REIT as a whole, we will be looking at its historical performance over the last 3 years. This will give investors a view of its growth. We will be discussing on 3 main areas being:

- Operational Performance

- Historical Financial Performance

- Historical DPU

Operational Performance

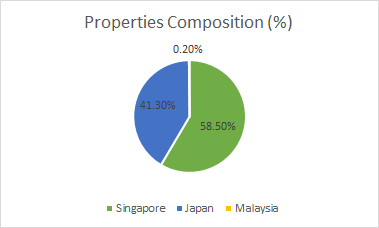

Parkway Life REIT owns 53 properties with a total asset under management of SGD 1.96 billion. From the total properties owned, approximately 99.80% of the properties relate to the assets in both Singapore and Japan. Both the assets in these regions have a committed occupancy of 100% as at 31 December 2019.

There are a number of key things to note of its Singapore healthcare assets which give it a slight edge. The properties are leased to Parkway Hospital Singapore Pte Ltd for a lease period of 15 + 15 years starting August 2007. This gives them a fairly secured rental income over these periods. There is also a positive rental reversion built-in on a yearly basis.

Secondly, the lease with Parkway Hospital is on a triple lease agreement basis. What it meant for Parkway Life REIT is that they do not need to bear these costs: property tax, property insurance, property operating expenses. This is another plus point as it will minimize its exposure to fluctuating operating expenses.

Its Japan healthcare assets, the second key region is performing rather well with a fairly strong outlook. They have entered in long term master lease with a weighted average expiry of 12.61 years as at 31 December 2019. These leases are entered on an “Up-Only” rental reversion basis.

Given the strong demand for healthcare in these regions especially during this period and the built-in positive rental reversion, we expect Parkway Life REIT operational performance to remain stable.

Strong year-on-year historical growth

| SGD in 000s | FY17 | FY18 | FY19 |

| Revenue | 109,881 | 112,838 | 115,222 |

| Net Property Income | 102,649 | 105,404 | 108,225 |

| Total return before changes in fair value | 82,043 | 85,081 | 86,549 |

The historical growth of Parkway Life REIT has been growing year on year over the last 3 years. The triple lease agreement of the leases plays a huge role in the minimal operating expenses fluctuation. Another key reason for the growth as explained in the point earlier is the built-in rental reversion of the properties in Singapore and the “Up only” rental review for its assets in Japan.

Given the uncertainty Covid-19 pandemic, we would expect that the demand for healthcare to be high. With that, healthcare REITs would be doing well during this period.

Growing Distribution Per Unit (DPU)

| Cents | FY17 | FY18 | FY19 |

| DPU | 13.35 | 12.87 | 13.19 |

| – Operations | 12.46 | 12.87 | 13.19 |

| – One-Off | 0.89 | – | – |

The third aspect we will be looking at is the DPU. If we were to look at the DPU over the past 3 years, you will notice a slight drop in FY18. This is mainly due to a one-off distribution to investors from the divestment its four Japan assets in December 2016 which was equally distributed over the four quarters in FY17.

Excluding that one-off gain, Parkway Life REIT has a rather stable and growing DPU from 12.46 cents in FY17 to 13.19 cents in FY19.

How does Parkway Life REIT perform amidst the pandemic?

From the few points earlier, you would have known that Parkway Life REIT has been performing well historically with a strong edge for growth. The question now is how does Parkway Life REIT perform amidst the Covid-19 pandemic. We always view healthcare REITs as a defensive REIT with a simple reason. Regardless of the economic cycle, there is always a demand for healthcare.

This is the same for Parkway Life REIT especially in the circumstances where they have a rather strong lease arrangement in the Singapore and Japan market. Let’s see if that is the case based on its 1H 2020 result.

Strong 1H 2020 Performance

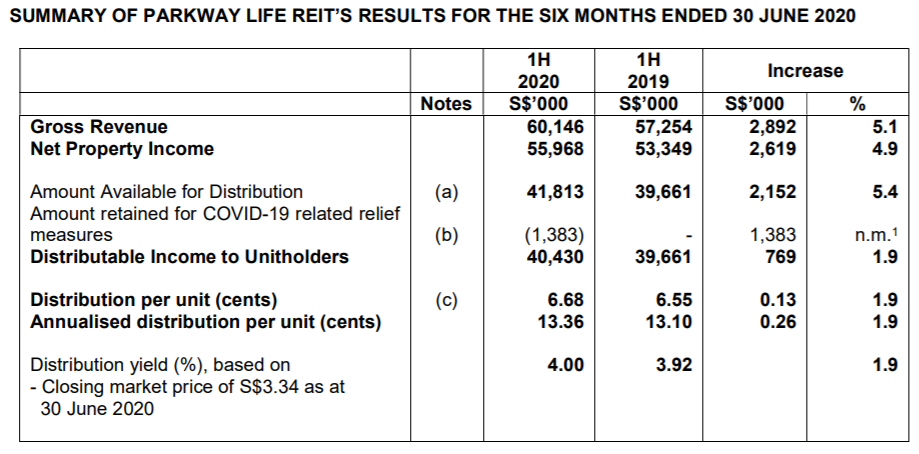

Based on the Q2 2020 Unaudited Result announced on 28th July 2020, Parkway Life REIT has been performing well amidst the Covid-19 pandemic. The revenue and net property income has increased by 5.1% and 4.9% respectively as compared to the similar 1st half in FY19. The growth is mainly attributed to revenue contribution from the Japan property acquisitions late FY19, higher rent from the existing properties and appreciation of the Japanese Yen.

There is not much disruption from the Covid-19 pandemic. The manager has retained SGD1.4 million as part of Covid-19 relief measure. Even with that retention, they have still managed to distribute 6.68 cents, a 1.9% increase in DPU to the investors.

Should you invest in Parkway Life REIT now?

Investing is a subjective matter and hence, do take this with a pinch of salt. Our verdict is Parkway Life REIT being a healthcare REIT is rather defensive in nature. They have a strong organic growth mechanism built-in for both its assets in Singapore and Japan. Its committed occupancy of 100% for both its strong region is another plus point.

Its defensive nature is well represented by its 1H 2020 result amidst the Covid-19 pandemic where it registered a positive financial performance.

Having said that, our verdict is that Parkway Life REIT is rather expensive. Based on its current trading price of SGD 3.56 and its NAV per unit of SGD 1.95 as at 31 December 2019, it would give investors a price to book ratio of 1.8.

Like what we have said earlier, investing is a subjective matter. Hence, it is important that you do your own due diligence before investing. If you are interested in healthcare REITs, you can check out other posts we have written previously on First REIT Performance and Al-Aqar REIT Performance.

Next week, we will be discussing and comparing the 3 healthcare REITs in Singapore and Malaysia. Do follow us on Facebook and Instagram to stay updated.

If you are just getting started, feel free to read more of our REIT Guide and REIT Analysis. You can also read more about what REITs are if you are new to REITs.

One Comment