Lendlease Global Commercial REIT (SGX: JYEU) or better known as Lendlease Global REIT is a REIT which was listed in the Singapore Exchange on 2 October 2019. They focus primarily on retail and office related assets. As at the date of this analysis, Lendlease Global REIT is traded at SGD 0.61.

Lendease Global REIT invest in two key properties being:

- 313@somerset which is located in Singapore

- Sky Complex, which comprises of three grade A office buildings located in Milan

| Valuation (SGD in mil) | Ownership | Proportion | |

| 313 Somerset | 1,008 | 100% | 70% |

| Sky Complex | 435 | 100% | 30% |

| Total | 1,443 | 100% | 100% |

As at 30 June 2020, both the property is valued at approximately SGD 1.4 billion with 313 Somerset accounting for 70% of the portfolio based on its property value. These properties are 100% owned by Lendleased Global REIT.

Given that Lendlease Global REIT was only recently listed, we will look at a few key things you need to know since its listing.

1) Long Lease with Sky Italia for Sky Complex

The first aspect we will look at is Sky Complex itself to give investors a flavour of what this property entails given that it is located in Milan. This asset is used mainly for commercial use being leased to Sky Italia for a term of 12 + 12 years with a lease expiry in May 2032. Definitely a plus point as it provides investors with a stable income over the lease term.

For those that do not know, Sky Italia is a British satellite television operated by Sky in Italy. It is a subsidiary of Comcast Corporation company (NASDAQ: CMCSA) which is global media and technology company.

Depending on how you view it, the fact that the lease is made with one master tenant can be detrimental if they decide to default given that they have the option right to break in 2026. However, investor can have some comfort given that Sky Italia is part of a major global company.

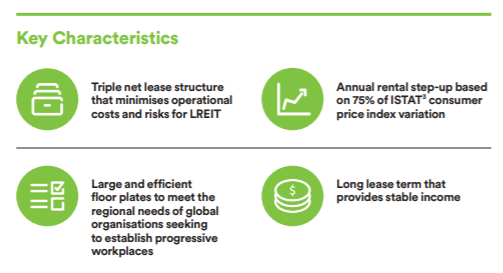

2) Build-in annual rental step-up and triple net lease arrangement for Sky Complex

The second aspect worth noting is the fact that the lease of Sky Complex is entered through a triple net lease arrangement. For those who do not know what this is, a triple net lease is an arrangement whereby the tenants would pay all the expenses of the property such as property maintenance, taxes, and insurance. This structure minimises the operational cost and risk for Lendlease Global REIT.

Furthermore, the lease is entered with an annual rental step-up based on the consumer price index variation. Another positive aspect of Sky Complex as it factor in the element of organic growth to the REIT.

3) Strong Support from Lendlease Group

The sponsor of Lendlease Global REIT is Lendlease group which is a multinational construction, property and infrastructure company listed in the Australian Stock Exchange. They have operations in Australia, Asia, Europe and the Americas. As at 30 June 2020, they have a development pipeline value approaching AUD 113 billion, core construction backlog of AUD 14 billion and funds under management of AUD 36 billion.

With a strong backing from a sponsor who are well versed in the real estate industry, this is definitely a plus for Lendlease Global REIT as well.

4) Strong Occupancy Rate of both Property

| Occupancy Rate | FY19 (IPO info) | FY20 |

| 313 Somerset | 99.6% | 97.8% |

| Sky Complex | 100.0% | 100.0% |

| Average | 99.9% | 99.5% |

In terms of operational performance of both these properties, there is a lack of comparative information to look at. Looking at FY20, its occupancy remain fairly high at above 99%. Though there is a slight drop as compared to the FY19 occupancy rate as disclosed in the Prospectus, the occupancy rate still remain healthy.

The drop is attributed by 313 Somerset. Despite the slight drop from 99.6% in FY19 to 97.8% in FY20, this is still fairly healthy given that it has been a challenging period for Singapore retail market. The REIT manager has shared that the average occupancy rate in Orchard Road is is approximately 91%. This is an indicator that 313 Somerset is performing above average operationally.

5) Financial Performance Review

We usually compare the financial performance across FY to get a gauge on how the REIT has perform but as the REIT was just listed late last year, there is limited comparative information. The financial forecast on the other hand is no longer relevant with the impact from COVID-19. Hence, in this segment we will discuss on the financial metrics solely based on FY20 information.

| SGD in 000s | Singapore | Milan | Total |

| Gross Revenue | 36,844 | 18,692 | 55,536 |

| Net Property Income | 23,410 | 16,879 | 40,289 |

| (Loss)/ Profit after tax | (28,453) | 19,837 | (8,616) |

| Amount available for distribution | n.a | n.a | 35,672 |

If you were to look at the table above, Lendlease Global REIT reported a loss after tax of SGD 8.6 million in FY20. The loss mainly relates to non cash items such as fair value loss of investment properties.

Throughout the entire year, the office sector remain resilience. The REIT manager still continues to collect full rental income in respect to the Sky Complex which can be sen from the profit after tax of SGD 19.8 million in FY20. Furthermore, the triple net lease arrangement of Sky Complex has allowed Lendlease Global REIT to minimize its operational cost and risk.

313 Somerset on the other hand, is not performing as well due to the COVID-19 pandemic. The circuit breaker measure along with the global travel restriction have affected businesses adversely. To help combat this, various support measure have been provided to tenants which is the reason of the drop in the Singapore asset.

6) Distribution Per Unit (DPU)

Looking at the distribution per unit of FY20, Lendlease Global REIT declare a total of 3.05 cents which is below their forecast. The lower DPU is contributed by 313 Somerset lower performance due to COVID-19 pandemic as shared in the previous point.

With the gradual easing of measures, we would expect the performance in 313 Somerset to slowly pick up.

7) Healthy Leverage Limit

The debt profile of Lendlease Global lease is relatively healthy. Its gearing level is at 35.1% which is way below the permissible limit of 45% (with a recent announcement to increase the limit to 50%). This would give them the headroom for further acquisition opportunities.

Read More: How does Interest Rate Affect REITs

Summary:

From our analysis, Lendlease Global REIT financial performance has definitely been affected by the COVID-19 pandemic given that their retail sector account for a bigger proportion of their asset. The asset in Milan remain resilience which is a favourable point for the REIT manager, provided that Sky Italia do not default or break the lease. This would secure Lendlease Global REIT a stable income till 2032.

With the gradual easing of measures in Singapore, investors should keep a look out on 313 Somerset to see if the performance improved.

What are your thoughts on Lendlease Global REIT? If you are just getting started, feel free to read more of our REIT Guide and REIT Analysis. You can also read more about what REITs are if you are new to REITs.

Do join our community over at Facebook and Instagram.